Abatable’s Head of Carbon Solutions, APAC, Bryan McCann, outlines the state of play for carbon markets in Asia and unpacks how three schemes compare on their requirements for eligible carbon projects.

Asia’s carbon compliance landscape is taking shape. Singapore’s Carbon Tax cost increased this year, Japan has recently launched its GX Emissions Trading System (GX-ETS) and airlines in the region are advancing their CORSIA strategies as the First Phase compliance deadline looms (31 January 2028).

In this article, we compare the different programmes and ask what they mean for the future of regulated carbon pricing.

Key takeaways

- Singapore, Japan, and international aviation each have a different carbon market compliance mechanism – CORSIA, Singapore’s International Carbon Credit Framework, and Japan’s Joint Crediting Mechanism – which are all underpinned by Article 6 of the Paris Agreement

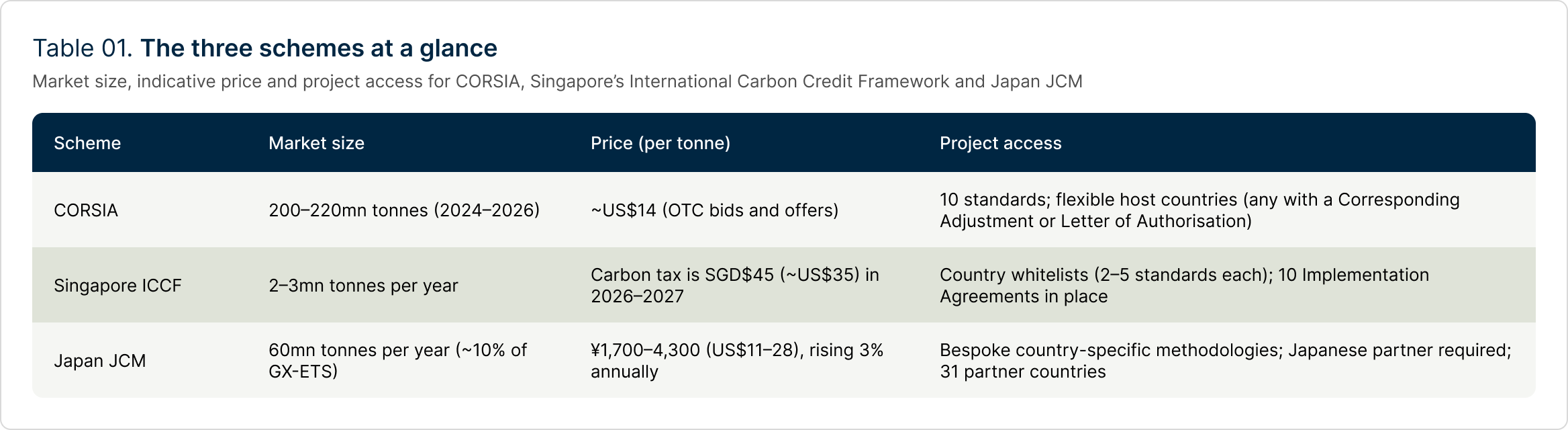

- CORSIA is the largest source of demand, with 200-220mn tonnes needed for its 2024-2026 First Phase. The scheme is the most flexible in terms of eligible methodologies and project host countries

- Singapore’s scheme makes it attractive for obligated entities to purchase international credits, but it limits supply to fewer than a dozen partner countries with Implementation Agreements

- Japan’s JCM has a 60mn tonne per year market, but its bespoke methodologies and Japanese partner requirements currently constrain eligible projects

Background

Under the Paris Agreement on climate change, countries set out a Nationally Determined Contribution (NDC) – their own country-specific climate target which is revised at five-year intervals. Article 6 of the Paris Agreement allows countries to meet their NDCs through international carbon trading.

This allows countries like Singapore – which face significant geographical barriers to reduce its domestic emissions – to fund climate mitigation elsewhere. Singapore, or companies operating in Singapore, can fund a climate mitigation project in Ghana, for example. In exchange Singapore receives some of the mitigation outcome to use against its NDC, known as International Mitigation Outcomes, or ITMOs.

Ghana then deducts the climate mitigation from its own emissions inventory by applying what’s called a Corresponding Adjustment (CA).

Carbon compliance markets that allow companies to use these international mitigation units require the units to be Correspondingly Adjusted. Buyer countries have flexibility on how they set up their international trading systems. Some, like Singapore, may choose to align closely with existing voluntary carbon market (VCM) registries and infrastructure. Others, like Japan, may build something more bespoke. Additional to national compliance market is international aviation’s carbon market, CORSIA, which will be the largest such market for Correspondingly Adjusted credits for the foreseeable future.

This article compares three key markets for ITMOs in East Asia: CORSIA, Singapore, and Japan.

Will programmes ‘converge’ with the voluntary market, as some have suggested, or at least complement the VCM and one another? Or will they be mutually exclusive and limit carbon project developers that are supplying credits to choose between them?

The convergence model: CORSIA First Phase

CORSIA – the Carbon Offsetting and Reduction Scheme for International Aviation – is a mandatory carbon offsetting programme for international airlines. Its goal is to neutralise the aviation sector’s growth above a 2019 baseline through the use of carbon credits. Abatable has estimated the total demand for CORSIA’s First Phase, covering 2024-2026 – at 200-220 million tonnes.

The scheme’s governing body, the International Civil Aviation Organization (ICAO), has embraced a high level of flexibility in the kinds of credits that are eligible under CORSIA, building on voluntary market infrastructure and standards such as Verra and Gold Standard. In this way, there is ‘convergence’ between CORSIA, a compliance program, and the voluntary market, though with important differences in the types of credits that can be purchased.

The credits – CORSIA Eligible Emissions Units – can currently be developed and issued under ten different standards for the 2024-2026 period. While CORSIA excludes some methodologies, and credit vintages need to be 2020 or newer, there is significant flexibility for project development.

For a credit to be fully CORSIA eligible to be used by an airline for its obligations under the scheme, it must:

- Use an eligible standard and methodology*

- Be from a project started after 2016 and with a credit vintage newer than 2020

- Have received a Corresponding Adjustment from its project’s host government, or received a Letter of Authorisation (LOA) which is underpinned by insurance against the government revoking the CA.

Organisations developing carbon projects for CORSIA thus have two priorities: implementing the project, and receiving a CA or LoA. Both can be challenging. But under CORSIA, project developers at least have considerable flexibility in the types of projects they can undertake and the countries in which they operate.

CORSIA builds on existing VCM infrastructure. Its methodologies, standards, registries, and even projects are the same. The major difference is requiring a CA, which, while challenging, is not insurmountable. To date, over 37mn carbon credits have received a CA and become fully CORSIA eligible, allowing airlines to actively start evaluating the market.

Because CORSIA market demand amounts to hundreds of millions of tonnes, it should be seen as the starting point for international compliance demand.

The complementary approach: Singapore’s International Carbon Credit Framework

Once Article 6 was operationalised at COP26 in Glasgow, Singapore quickly established a strong framework to import credits for its own climate targets.

It has provided two pathways for procurement:

- Direct procurement, through the Singapore government launching Requests for Proposals for the purchase of credits, paid with government funds.

- Under its carbon tax, giving tax liable entities the option to meet up to 5% of their requirements by using eligible credits.For the country, this offers a self-reinforcing approach to purchasing: the government provides a political signal through public and large-scale tenders, and the tax-liable entities can explore different commercial structures or approaches to project investment.

Singapore designed its system as ‘CORSIA-plus’, taking the basic structure of CORSIA and including additional requirements.

Singapore’s main limiting factor, however, is based on the host country of the credits it purchases.

Under Article 6, bilateral cooperative approaches often involve an agreement between the buyer country (Singapore) and the seller country (for example, Ghana). While Singapore has signed over 20 Memoranda of Understanding with host countries since 2021, it was not until mid-2025 that it formalised these into Implementation Agreements under which credits can be transacted.

As of 28 April 2026, Singapore has 14 MOUs and 10 Implementation Agreements in place.

Compared with CORSIA, requiring a host country implementation agreement is significantly more limiting. This takes the programme from potentially hundreds of host countries in the CORSIA case to fewer than a dozen.

Each Implementation Agreement has two crucial components:

- An eligibility ‘whitelist’ denoting the different standards and methodologies which can be used to develop projects.

- A multi-stage approval process for developers to go through.

These will differ by country, though there is an effort to standardise and streamline to the extent possible. Some countries – like Ghana – have just Verra and Gold Standard on the whitelist. Others, like Bhutan, can have as many as five**. In either case, this is more limiting than the ten standards usable under CORSIA, and creates complexity as they differ country-to-country.

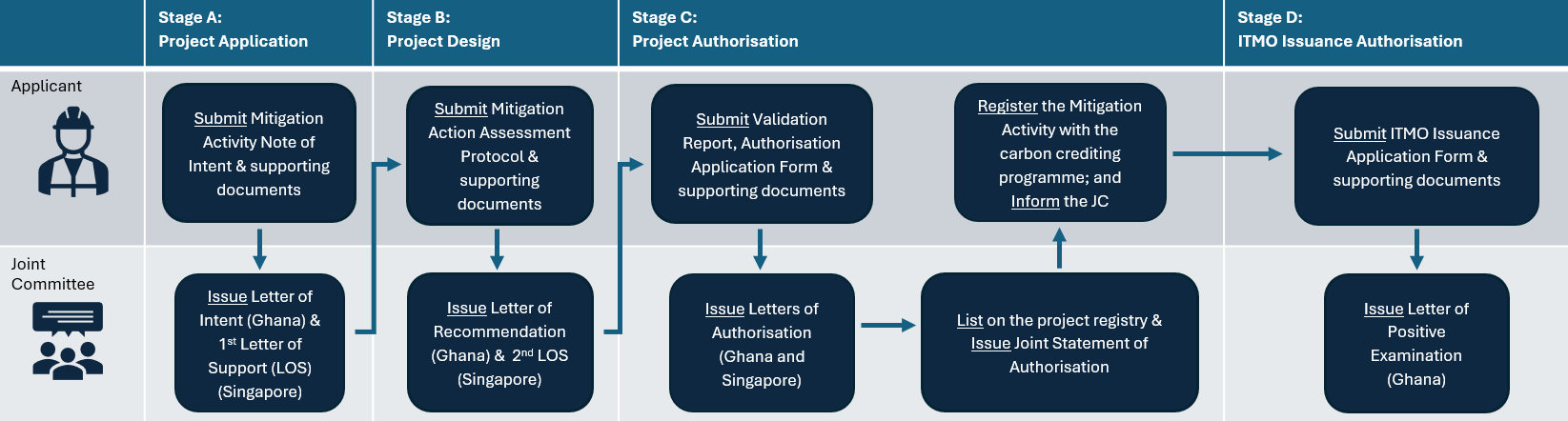

Figure 1. Singapore’s multi-stage approval process for project developers. Source: Singapore’s Carbon Markets Cooperation

The approval process also creates further uncertainty regarding when their projects will progress through various stages. For Ghana, there are four stages at which different documents must be provided (see Figure 1).

The benefit of Singapore’s programme, however, is price and demand certainty. Singapore’s 2024 BTR included a target of 12.56mn international credits purchased from 2026-2030. The country’s carbon tax is SGD$45 (approximately US$35) per tonne in 2026 and 2027, meaning there is an incentive for companies to purchase international credits, which will likely be at a discount to the tax rate.

Singapore’s tax rate is more than double the current traded CORSIA price (at time of writing, approximately US$14 per tonne based on over-the-counter bids and offers), and is set through government fiat rather than purely from supply and demand.

While Singapore’s market is only 2-3mn tonnes per year, it provides a complementary model for carbon project developers working in CORSIA. The methodologies are the same, and while there are fewer eligible host countries, many of the states with which Singapore has signed agreements are the most ready to apply CAs.

Singapore has made the conscious choice to build from existing market infrastructure, as CORSIA has, removing a potential barrier to supply under its scheme.

Building from the ground up: Japan’s Joint Crediting Mechanism

Japan’s Joint Crediting Mechanism (JCM) offers a contrasting approach to both CORSIA and Singapore’s framework. Launched in 2010, the JCM is a made-in-Japan complement to the 1990s-era Clean Development Mechanism (CDM), established under the Kyoto Protocol.

Like Singapore, Japan has limited capacity for domestic climate mitigation – it is a mountainous and densely populated island country with a significant heavy manufacturing sector. The Japanese government aims to generate 100mn tonnes of CO2 reductions through the JCM by 2030, scaling to 200mn by 2040.

Like Singapore, Japan relies on formal government-to-government partnerships. Japan has signed agreements with 31 partner countries as of January 2026, of which 20 are now Article 6 compliant; the rest predate the Paris Agreement and need updating

A major point of divergence lies in the underlying market infrastructure. Both CORSIA and Singapore have made conscious choices to build upon existing voluntary market standards, such as Verra or Gold Standard, offering eligible ‘whitelists’ of external methodologies that can be used.

By contrast, the JCM has traditionally relied on its own bespoke architecture governed by joint committees formed between Japan and the host country. The JCM requires that each of these joint committees approve each methodology independently. Therefore, rather than have one global methodology for clean cooking, for example, the JCM requires a new methodology to be created and approved for each country.

While many of these ‘country-specific’ methodologies are reusing CDM approaches, approvals still take time, particularly for more complex project types such as forestry and agriculture. So far, there have been 107 approved methodologies across various sectors.

Projects also require a Japanese partner alongside the developer in the host country, increasing complexity. Finally, similar to the Singapore approach, projects must be approved individually. This includes determining on a project-by-project basis the share of emissions reductions that stay with the host country versus being exported to Japan.

These constraints on supply are reflected in the number of projects. Despite its inception 15 years ago, there have been under a million tonnes issued.

However, there are unique strengths to Japan’s position in the international market.

The first is direct government project support. Originally, the JCM was a government-led programme. Organisations like the Japan International Cooperation Agency (JICA) funded a series of pilots, with companies awarded JCM subsidies eligible to finance up to half the investment cost of approved projects.

In 2023, the JCM was expanded to allow for private sector project development, with credits sold into the GX-ETS, Japan’s emissions trading programme. This is a second strength: market size, estimated at 60mn tonnes per year, 10% of the estimated 600mn tonnes covered under the GX ETS.

Finally, pricing in the GX-ETS is set at a band between ¥1,700 Japanese yen and ¥4,300 Japanese yen (USD$11-USD$28) per tonne of CO2, with prices increasing by 3% each year. While less than Singapore, this is comparable to pricing in CORSIA and well in excess of the voluntary market.

Government subsidies, substantial market size, and healthy pricing make JCM an attractive market. However, the programme’s complexity and the requirements for developing new methodologies make it difficult to scale supply. Discussions are ongoing regarding the JCM streamlining approaches to allow existing projects developed using international methodologies to ‘dual-list’ under the JCM, or to allow for licensing of international methodologies. Either of these enhancements to the programme would lower barriers to access for carbon project developers.

So, what should investors and developers choose to do?

Project developers face a set of choices when developing new projects for East Asian compliance markets.

CORSIA is effectively the default international compliance market that buyers in East Asia, and globally, are engaged in. It has the largest volume, and the most flexible set of methodologies and host countries. If a project developer has the right relationships in the right countries and can access CAs, it can develop conventional voluntary projects, make them CORSIA eligible, and receive a significant price premium.

Alternatively, if a project developer is in one of the Singapore partner countries, it can develop a project for that market instead, while still retaining market optionality. If it cannot find a buyer, the project can readily be resold in CORSIA (provided a CA allows for that) and, if it cannot get approval, the project can be sold in the voluntary market.

Under its current design, Japan’s JCM is the most restrictive of the three. Despite the market’s size and pricing level, projects must be developed using a bespoke methodology with a Japanese partner. Should a project fail to receive approval, or to find buyers, developers are potentially left with a project that cannot readily be transitioned into CORSIA or the voluntary market.

These are just three examples of different crediting approaches for compliance schemes. Other countries, such as Switzerland, Sweden, and South Korea, are considering different bilateral approaches. And to add a further layer, the Paris Agreement also includes another mechanism for crediting, aptly known as the ‘Paris Agreement Crediting Mechanism’: run centrally under the United Nations. While we do not have time to go into this mechanism here, it could provide a global, standardised alternative to a ballooning array of bilateral approaches.

‘International carbon markets need more ambition, action, and innovation. Countries like Singapore and Japan are pioneering ambitious bilateral approaches, with CORSIA creating a deep pool of demand to underpin investment.

Abatable, as a leading market advisor and procurement platform, helps organisations operate in these new compliance markets. Get in touch if you’d like to talk through your strategy.

* As of April 2026, the ten standards eligible for the 2024-2026 phase of CORSIA are the American Carbon Registry (ACR), Architecture for REDD+ Transactions (ART), BioCarbon Fund for Sustainable Forest Landscapes (ISFL), Climate Action Reserve (CAR), Forest Carbon Partnership Facility (FCPF), Global Carbon Council (GCC), Gold Standard (GS), Isometric, Premium Thailand Voluntary Emission Reduction Program (Premium T-VER), and the Verified Carbon Standard (VCS).

** Gold Standard for the Global Goals, Verified Carbon Standard, American Carbon Registry, Global Carbon Council, and the Architecture for REDD+ Transactions